GO TO 2040 calls on CMAP to track indicators and set targets on the efficiency, equity, and transparency of the state and local tax system. This is the second in a series of Policy Updates that will examine CMAP's tax policy indicators. This post outlines how CMAP views tax system equity. A previous post examined efficiency, and a future post will examine tax system transparency.

Equity of the tax system includes two components. Horizontal equity in the tax system means similar people and firms should share similar burdens. Vertical equity means that the tax system should be based on the entity's ability to pay. By this same token, the tax system should also ensure that local governments have the ability to fund services. If communities are unable to raise revenues needed for the provision of public services that help attract residents and businesses, it may hinder the economic growth of the region as a whole. In addition, low tax bases have the effect of driving up tax rates, which results in a cycle of low economic growth.

Since most local governments depend on revenues like property and sales taxes to fund basic services, CMAP's regional tax policy indicator for equity will use a measure of the tax base equal to the sum of a municipality's equalized assessed value and retail sales per capita. In 2012, the median per capita tax base was $42,322, meaning that half of the municipalities in the region had between $4,234 and $42,322 in sales and property tax base per resident, while the other half had between $42,322 and $1.3 million.

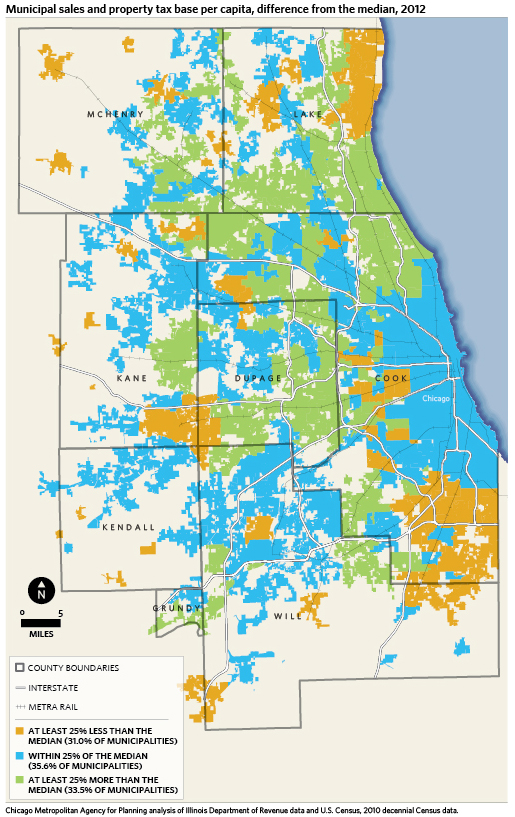

Divergence from the Median Per Capita Tax Base

While a plurality of the region's municipalities have a per capita tax base that is within 25 percent of the median, approximately one-third of the region's municipalities have a per capita property and sales tax base that was at least 25-percent lower than the median. The proportion of communities at this level of low capacity has also remained relatively stable over the past ten years, ranging from 28 percent to 33 percent. Similarly in 2012, 33.5 percent of communities had a per capita tax base that was higher than the median by at least 25 percent. The following map provides an overview of per capita tax base by municipality for 2012, shown by difference from the median.

Click for larger image.

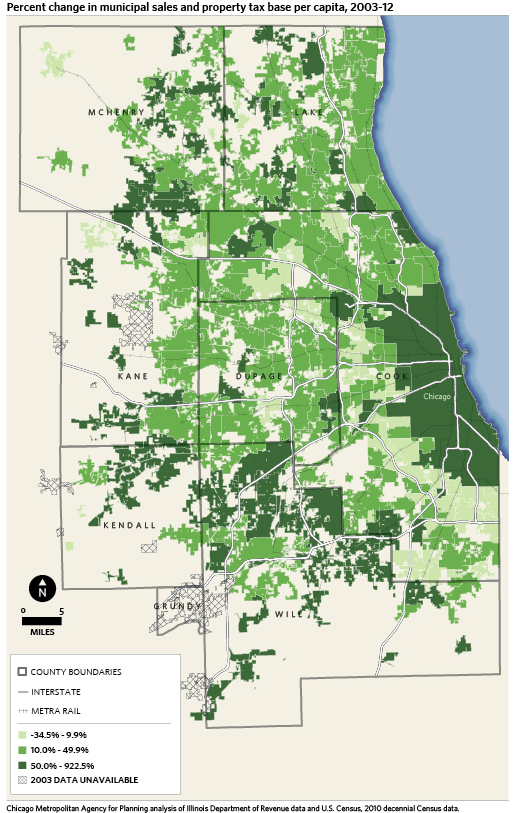

Change in Per Capita Tax Base

Several of the municipalities with a low tax base have also experienced low per capita tax base growth, or even declines, over the past ten years. A low tax base can contribute to high property tax rates, which can discourage economic development. As a result, some communities with low tax bases fall into a cycle of low economic growth. The following map provides an overview of the percent change in sales and property tax base per capita between 2003-12 by municipality.

Click for larger image.

Targets for Equity of the Tax System

While there will always be communities with smaller tax bases than others, implementing the recommendations of GO TO 2040 can help reduce the proportion of communities with a low tax capacity. Today, 31 percent of the region's communities have a significantly lower tax capacity than the median, and this has not changed significantly over the past decade. However, in 2040, CMAP projects that this number could be lowered by roughly half to 16 percent.

Click for larger image.

Conclusion

GO TO 2040 recommends a series of broader regional efforts to provide economic development opportunities to all communities. The plan recommends reinvestment in our existing communities, strategic infrastructure investment, and more targeted education and workforce strategies to prepare the region's labor pool for the jobs of the 21st Century. These types of investments should serve to encourage economic development activities in lower capacity communities.

Additionally, GO TO 2040 and CMAP's Regional Tax Policy Task Force have emphasized some specific tax policy reforms to help enhance the tax bases of municipalities that might be struggling to generate the revenue necessary to provide services. Potential ways to enhance the property tax base of some municipalities include eliminating property tax assessment classification in Cook County, which would make many of these communities more conducive to economic development. In addition, new approaches to allocating state sales tax revenue to municipalities could also help to ensure that economically depressed communities have the revenues necessary to provide public services.